___________________________________________________________________________________________

China’s domestic timber supply has historically been of limited relevance to Chinese importers of logs and sawn timber. Supply was relatively scarce, particularly in rapidly developing regions, while demand was strong. This allowed imported supply to dominate the market. More recently, however, domestic supply has become more visible, and in certain areas and applications has been displacing imported timber.

However, China's reliance on imports has not aligned well with China’s strong policy emphasis of self-reliance. As a result, the country has invested heavily in expanding its forest areas, particularly in the southwest, south-central, and southeastern parts of the country. These forests are now reaching harvest age and are increasingly being harvested.

Total domestic production has increased from approximately 100 million m³ in 2020 to nearly140 million m³ in 2024. Most of this growth has been in the southeast,especially in Guangdong and Guangxi. The southeast has emerged as the most important timber producing region, and now accounts for over 50% of China’s domestic timber supply.

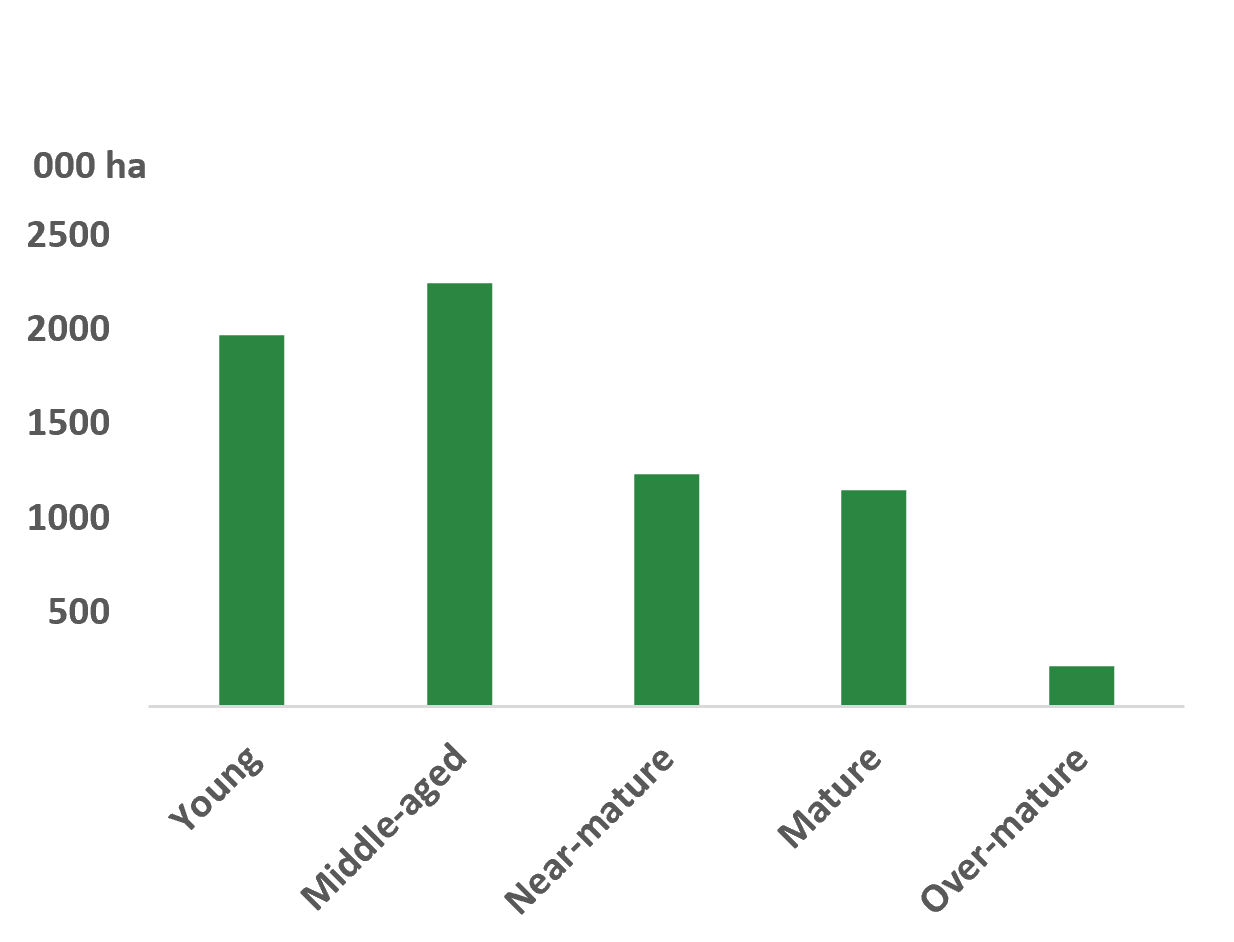

Figure 1. Forest Area By Maturity Class in Southeast China

The plantation forests consist predominantly of Eucalyptus, although softwoods such as Masson pine and Chinese fir have also been widely planted. In the southeast alone, plantations of pine and fir cover more than 7 million hectares—around four times the total plantation area of New Zealand.

The species composition of these plantations is highly relevant to market dynamics. Most Eucalyptus is better suited to pulp, reconstituted wood products, and lower-grade veneers. As such, it has had limited impact on markets for imported timber which is used in construction, plywood, packaging, and furniture. In contrast, most of the competition for imported logs comes from Masson pine and Chinese fir.

China’s softwood plantations are relatively young, with a large proportion of areas in younger and mid-rotation age classes. This suggests that domestic softwood supply is likely to increase. Based on the current age-class distribution, potentially production could double over the medium term as these forests mature.

Figure 2. Forest Area By Maturity

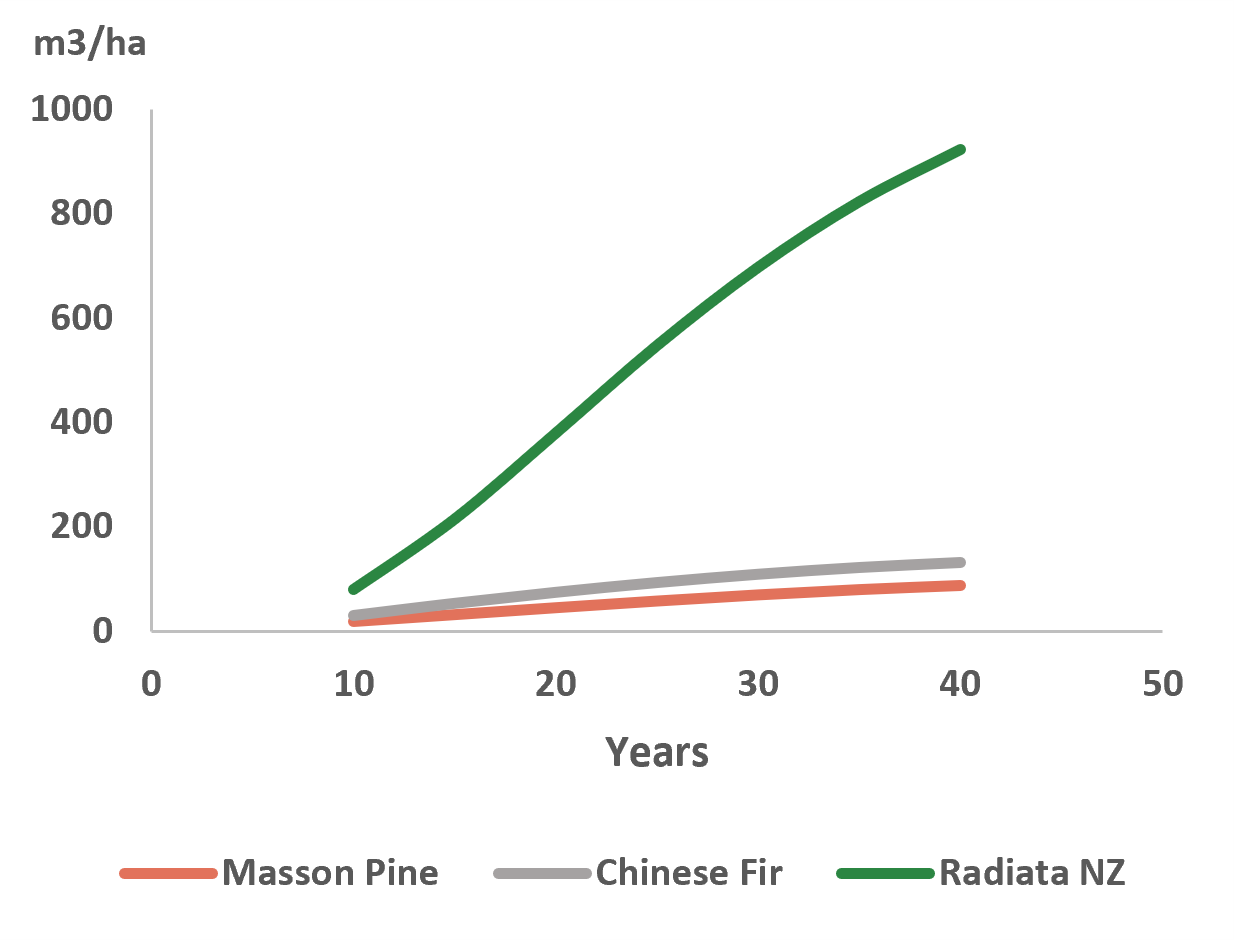

Productivity in China’s softwood plantations is significantly lower than in New Zealand and other major forestry regions. Yield curves indicate that Masson pine and Chinese fir typically reach volumes of around 80 to 120 m³ per hectare at age 30. By comparison, over the same period radiata pine in New Zealand can achieve approximately 700 m³ per hectare.

Growth rates of the pine and fir begin to slow after around 15 years, with mean annual increment (MAI) peaking at approximately age 25. As a result, extending rotations much beyond this point is generally uneconomic.

These factors result in an average log profile that is substantially smaller than that of New Zealand forests. Anecdotal evidence suggests that only about one-third of Chinese logs exceed 14 cm indiameter—roughly the minimum size required for New Zealand export markets. While China's forests do produce larger logs, the volumes are relatively limited.

Figure 3. Stand Growth

Log quality is also influenced by factors such as stem straightness, taper, and fibre characteristics. Masson pine, for example, is highly resinous, and many stands are affected by resin tapping, which can reduce wood quality. Logs are also generally shorter than radiata pine due to poorer stem form.

More generally, pine and fir forests in southern China face a number of challenges, including relatively low productivity, variable quality, and limited structural diversity.

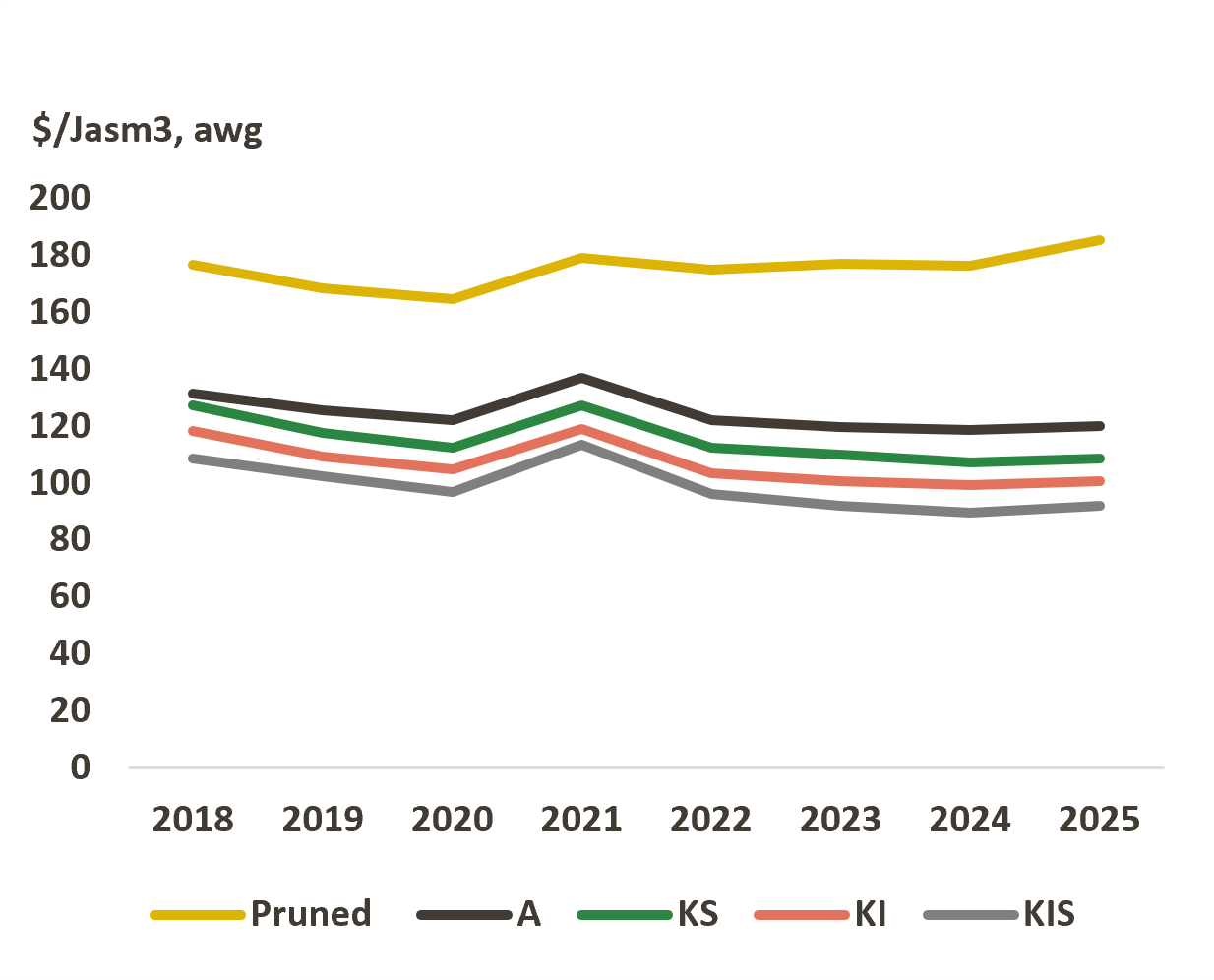

Figure 4. NZ Log Export Prices

The expansion of China’s domestic softwood supply does not simply result in a direct substitution of imports. Differences in log size and quality have led to distinct patterns of use.

Domestic timber is increasingly being used in reconstituted wood products, lower-grade construction applications, and core veneer in products such as plywood and laminated veneer lumber.

For imported radiata pine, the most direct competition is in the smaller-diameter and lower quality log classes,such as those of KIS, KI, and short K grade.

After many years of relatively narrow price differentials, a widening gap between lower- and higher-quality logs is likely to emerge. Price differentiation between shorter and longer logs is also expected to increase. The growth in China’s domestic timber supply will have important implications for international suppliers. In particular, it is likely to influence log pricing structures, increase market differentiation, and affect how forest assets are managed and valued in exporting countries such as New Zealand.